-

Advisers are reassessing their approach to retirement income as annuities make a comeback

-

Uncertainty among investors points to the enduring value of advice at retirement

-

Advised clients remain more confident about their retirement plans than their advisers

New economic age, new options for retirement income?

A shifting approach to retirement income

Since the 2015 pensions freedom reforms, income drawdown has been the dominant approach to retirement income among advisers, but annuities are back. A regime change in the economic environment to one of higher interest rates and higher bond yields has made annuities an attractive option again.

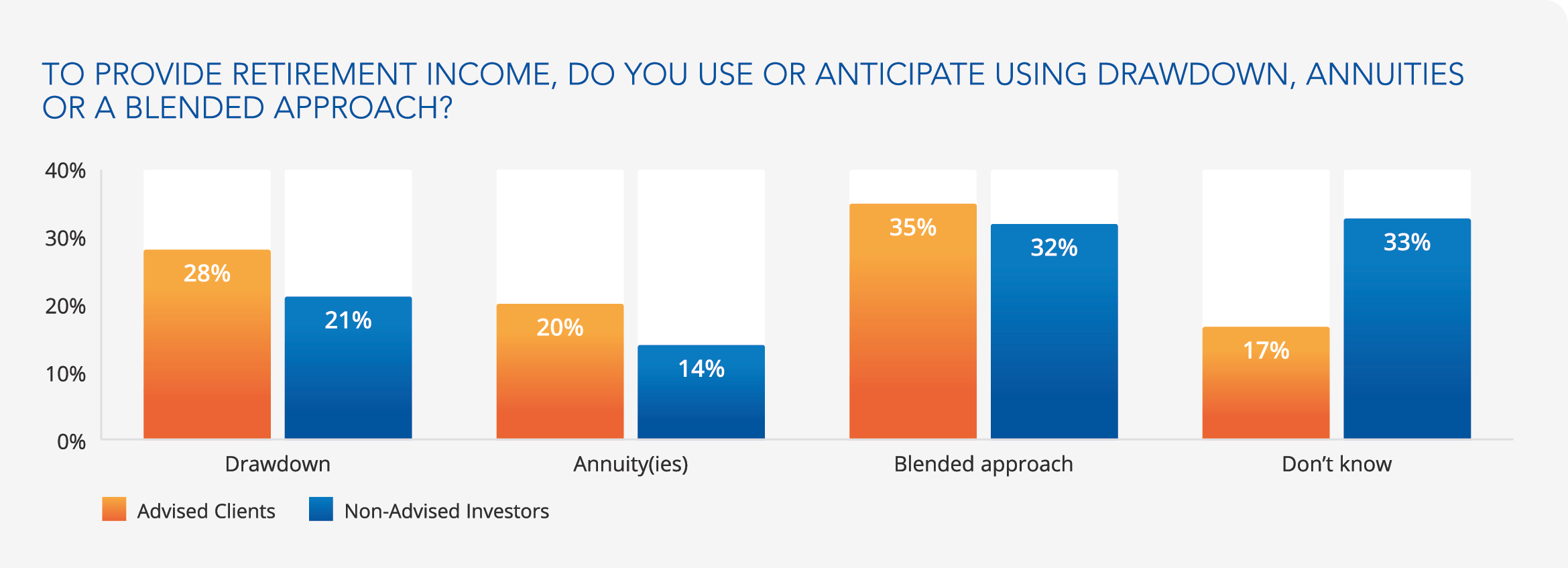

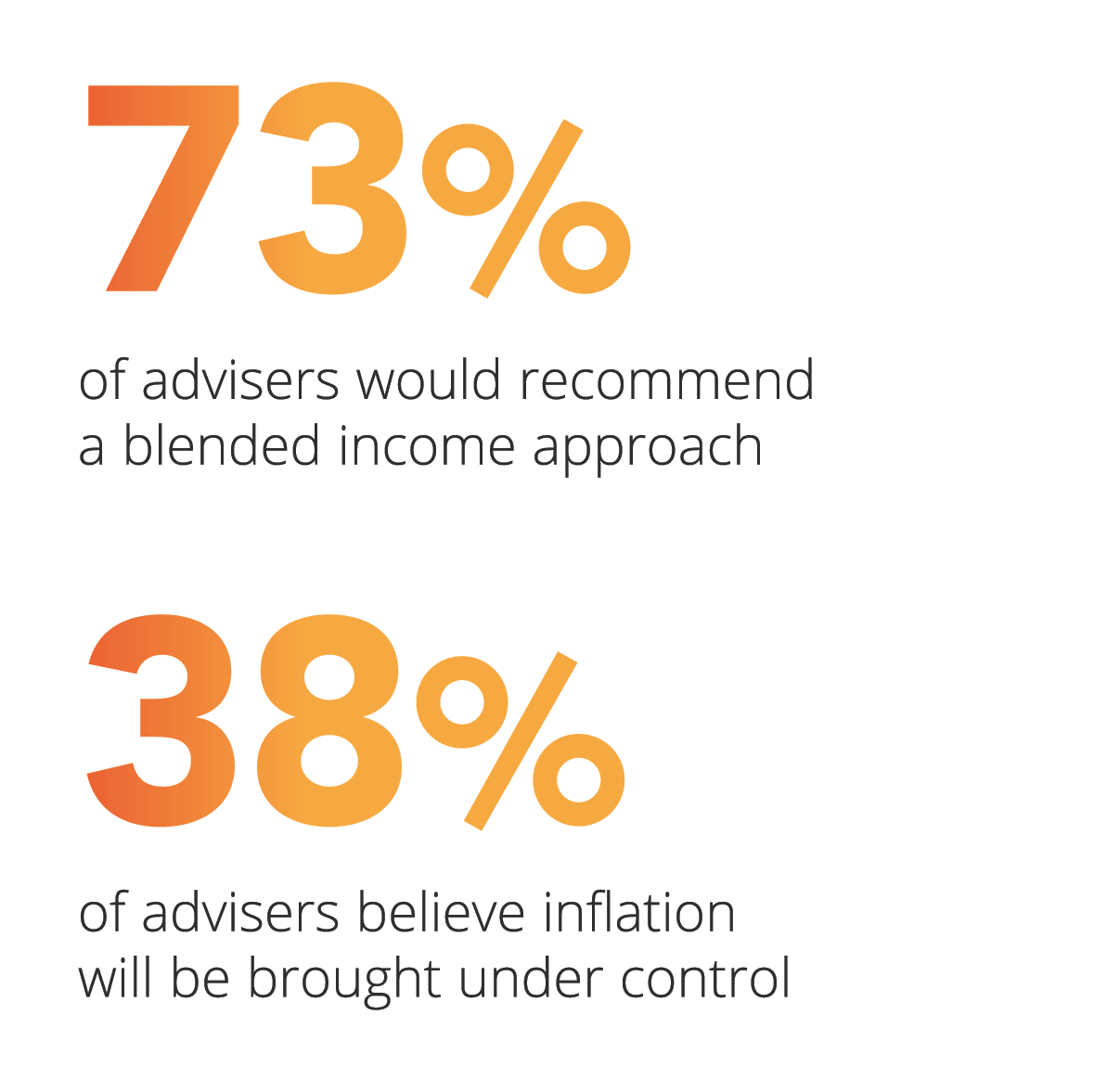

As a result, 73% of advisers would now consider a blended approach to retirement income for the majority of their clients, which combines the continuing growth potential of flexible income drawdown with the ability to annuitize part of the pension fund.

Interestingly, a firm 88% majority of advisers fear that the rise in annuity rates could simplify retirement choices. Yet, our survey suggests that fear could be overdone, as investors reported high levels of uncertainty when asked to select a retirement income route. While the blended approach came out on top for all investors, a third (33%) of non-advised investors are unsure about which approach to use. Encouragingly, only 17% of advised investors are uncertain, highlighting the benefits of advice and the greater financial confidence advisers can instil in their clients.

It’s not just about annuity rates. The other side of the coin is shifting consumer priorities. Due to rises in the cost of living, greater numbers of investors now want the certainty and peace of mind provided by a guaranteed level of income that can match their higher monthly outgoings. Over a third (34%) of advised clients told us they have reduced their investment contributions (ISA/GIA) due to the higher cost of living, while one in five (20%) have reduced their pension contributions. It is for this reason that a defined level of income has moved up within some investors’ hierarchy of needs.

Lastly, higher interest rates and annuity rates could be sticky. Only 38% of advisers believe that central banks will bring inflation under control in the next three years. This new economic environment with a higher cost of living, combined with the impact of Consumer Duty and the FCA’s thematic review of retirement income augurs for continued strong use of the blended approach.

Revisiting retirement readiness

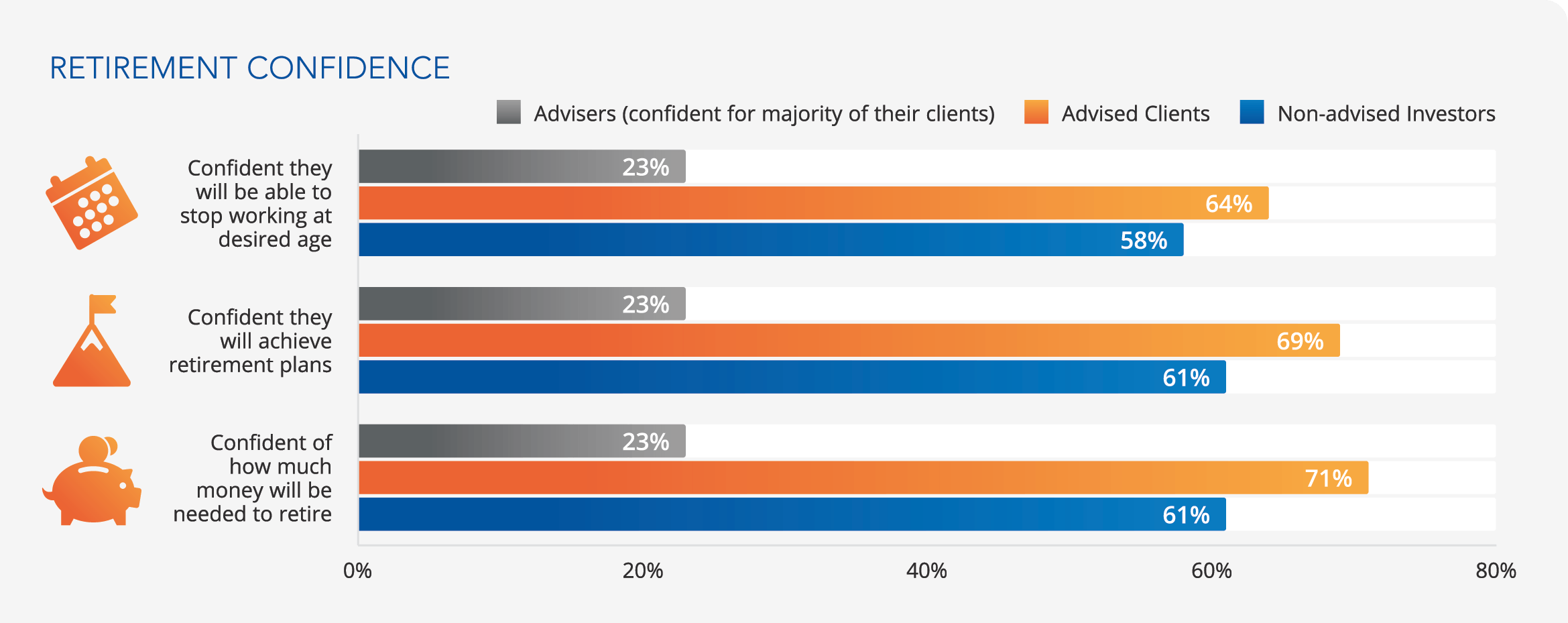

There are two noteworthy gaps on retirement readiness. The first is the greater confidence of advised clients over non-advised investors, which again speaks to the value of advice. Advised clients are notably more confident than non-advised clients that they will be able to stop working at the age they want, that they will be able to achieve their retirement plans and they know how much money they need to retire.

The second noteworthy gap is between advisers and investors. Retirement readiness remains a concern for advisers, especially in the present economic environment, with 22% of advised clients reporting they have reduced or will have to sell some investments to maintain their standard of living. Less than a quarter (23%) of advisers are confident that the majority of their clients will have enough in their portfolio to meet their retirement expectations; 31% believe half their clients will have enough, while 46% believe only a minority of their clients will have enough.

This concern does not carry over to investors, however. 69% of advised investors and 61% of non-advised investors are confident that they will still be able to reach their retirement goals. This confidence gap has been a long-established one in our survey. However, the fact that the gap persists in the face of the current cost of living challenges suggests there may be a degree of complacency or wishful thinking on the part of investors when it comes to retirement.

Given each investor’s expectations are specific to them, one way of closing this gap may lie in a more detailed exploration of their post-retirement lifestyle: the food, house, clothing, transport and holiday expenditures that they expect to make. The PLSA’s Retirement Living Standards* shows these costs for a minimum, moderate and comfortable level of retirement. That exploration could help with the finely balanced client conversations advisers may need to have with certain clients about maintaining their pension contribution levels.

* Source: www.retirementlivingstandards.org.uk

“Attractive annuity rates and innovations in product design to allow a blended approach to

retirement income have put a new focus on adviser-client retirement conversations. Even for

clients with larger funds, advisers are increasingly discussing the option of securing defined

levels of guaranteed income at their annual drawdown reviews. The blended approach allows

advisers to offer appropriate clients a best of both worlds mix of security and flexibility: the

peace of mind of knowing that living expenditures are covered by a guaranteed income, and

the ongoing growth and income generation potential that comes from having the rest of the

pension in flexible drawdown.”

Jamie Drewett

Head of Intermediary Sales, Embark Group

Download the full guide

Looking to download the full Embark Investor Confidence Barometer? Simply click the button and download the guide.

Key Insight 1

Are advisers under more pressure than ever?

Are advisers under more pressure than ever?

Key Insight 2

New economic age, new options for retirement income?

New economic age, new options for retirement income?

Key Insight 3

Do investors need saving from themselves?

Do investors need saving from themselves?

Key Insight 4

Can advice help close the gender retirement confidence gap?

Can advice help close the gender retirement confidence gap?